Are Business Executives Overpaid?

A team of MTSU's economics and finance faculty members is researching the trend in executive compensation measured as a percent of corporate profits.

by William Ford and Kevin Zhao*

| print pdf version |

During the current very serious economic recession, the financial media have focused a lot of attention on the compensation paid to top business executives. Numerous examples of multimillion-dollar payments to executives of failing companies that have received huge injections of taxpayer dollars have generated a firestorm of public protests. The U.S. Congress and President Obama's Cabinet members have also responded by initiating a series of actions designed to curtail excessive compensation payments to the executives of such companies. That, in turn, has rekindled interest among academic researchers in "agency theory."

Agency theory focuses on the question of how best to align the interests of shareholders of public companies with the inherently conflicting interests of non-owner managers. When a company is managed directly by its owners, economists assume there is no inherent economic conflict between the two roles of owner-managers. However, when the managers own little or none of the stock in a company, they may attempt to maximize their own compensation rather than their company's profits and dividends accruing to shareholders. And, in today's financial crisis environment, when taxpayer monies are used to rescue or nationalize failing companies such as Fannie Mae, Freddie Mac, General Motors, and AIG, media-driven public resentment rises when the top executives of such firms are seen flying around in corporate jets and drawing multimillion dollar salaries, bonuses and other benefits.

In response to this re-aroused interest in executive compensation and related agency-theory issues, a team of MTSU's economics and finance faculty members has initiated a project drawing on a number of databases to shed some new light on the question of whether or not non-owner business executives are, over time, capturing a growing share of the earnings of major publicly owned companies they manage. To address this issue, the MTSU team has developed a new metric, the executives' total compensation measured as a share of company earnings. Or, in plainer English, what is the trend in executive compensation measured as a percent of corporate profits?

In the first phase of work on this project, recently completed and published in the April 2009 issue of Business Economics, the MTSU team measured the "CEO Share of Earnings" (CEOSE) of S&P 500 companies over a 15-year period, from 1993 through 2007, the latest year for which data on those companies is available. During 2007, the CEOs of the S&P 500 companies in our sample varied in age from 38 to 83 with a median (mid-point) age of 56. Their companies, on average, had roughly 55,000 employees and $65 billion in assets. At the end of that year, the market value of the average company was about $30 billion, and the average CEO received total compensation of $10.8 million, of which only 10%, or about $1 million, was salary. The other 90% of the CEO's total compensation was received in bonus payments, option awards, restricted stock grants, and various other forms of compensation including private use of company planes, club memberships, professional tax advice, etc.

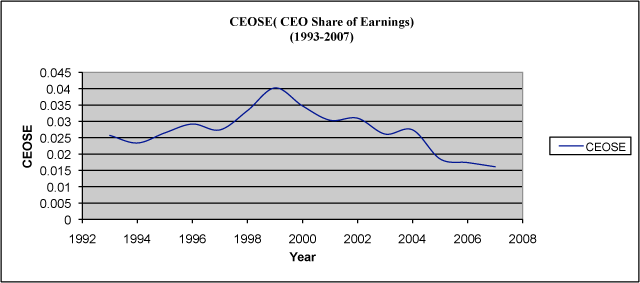

Measured as a share of corporate earnings (after-tax profits) the S&P 500 CEO's share of earnings (CEOSE) averaged about 2.4% over the entire 15 years from 1993 to 2007. As shown in Figure 1, the CEO share of earnings generally rose from around 2.5% in the mid-1990s to a peak level of 4.0% in 1999 and, surprisingly, has trended downward since then, ending at a historically low level of about 1.6% of earnings in 2007.

Figure 1. CEO Share of Earnings (1993-2007)

Source: Business Economics, April 2009, Vol. 44, No. 2, p. 122

Source: Business Economics, April 2009, Vol. 44, No. 2, p. 122

Moreover, during that entire period, CEOs' average salary, in inflation-adjusted dollars, rose by only about one-third of 1% annually, and their bonuses actually declined by over 1% per year. However, their total compensation rose by roughly 6.1% annually, driven mainly by restricted stock grants. Because almost all corporate stocks have declined sharply in value since the end of 2007, a majority of those restricted stock grants are undoubtedly now much less valuable than they were in 2007. The same is true of the stock option awards received in recent years by S&P 500 CEOs.

Readers of this article may, by now, be as intrigued as the authors were to find that this preliminary study of long-term trends in S&P 500 CEO total compensation is not consistent with the public's media-driven perception that top executives of U.S. companies are increasingly overpaid, at least not when their compensation is measured as a share of their companies' after-tax profits, CEOSE. And, as noted above, it is now virtually certain that CEOSE fell sharply in 2008. According to an Associated Press analysis of regulatory filings from 309 companies in the S&P 500, average CEO compensation fell 7% in 2008.

Unfortunately, our preliminary work does not directly address the current financial crisis and the current economic recession because the sample of companies we studied omitted S&P 500 firms that were merged out or failed and firms that were unprofitable during the period we analyzed. Also, our initial findings covered only the total compensation trends of the CEOs of S&P 500 companies.

Looking ahead, we plan to delve more deeply into trends in total executive compensation in a number of ways. For example, we will examine the total compensation of the top executive teams of S&P 500 companies rather than just trends in the CEOs' share of earnings. We also plan to refine the sample of companies we study by adjusting it for mergers that occurred over time and other factors that bias the sample of companies we used in this first pass at the databases we are using. Because most of the recent media and public concern about executive compensation has been focused mainly on financial companies, we also plan to conduct a separate study of the S&P 500 companies in that industry.

In conclusion, our preliminary answer to the question of whether business executives are overpaid is: perhaps not. If we assume that CEOs of major U.S. firms should be compensated based on the earnings they manage to produce for the shareholder owners of their companies, this first pass at long-term trends in their total compensation does not indicate that S&P 500 CEOs are receiving a growing share of their companies' profits over time. Whether or not that finding holds for major financial firms, or for top executives of failing firms supported by the taxpayers, remains to be seen.

* At MTSU, William Ford is a professor of finance and chairholder of the Weatherford Chair of Finance and Kevin Zhao is an assistant professor of finance.